|

Action required

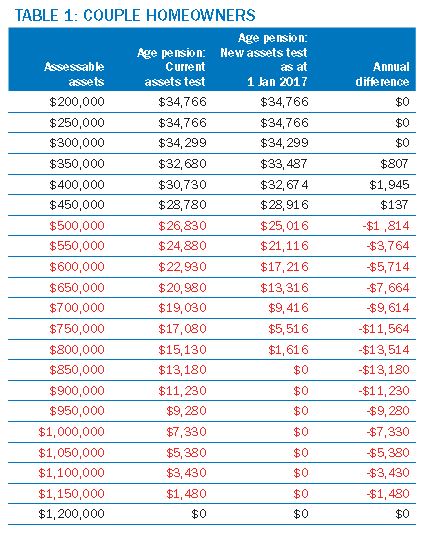

Clients that fall within the asset levels where they will see a fall in their ongoing Age Pension entitlements, the following options may be considered to help reduce their assessable assets:

- Purchase funeral bonds, up to $12,500, which are exempt from asset test assessment

- Buy a more expensive principal residence

- Undertake home improvements

- Pre-pay a holiday

- Gift up to $10,000 per financial year, or $30,000 over a rolling 5 year period

- Couples with a spouse under Age Pension age, may look to withdraw part of the older partner's super, and recontribute back into super for the younger spouse, to shelter these assets from assessment, until the younger partner reaches Age Pension age

- Purchase a lifetime annuity, which are assessed as 'long term income streams' that are not subject to deeming, and have a reducing asset value

Even with these strategies, some clients may be unable to sufficiently reduce their assessable assets to a level that would allow them to retain an Age Pension entitlement from 1 January 2017. Those clients will automatically be eligible for the Low Income Health Care Card, and those over Age Pension age will also be eligible for a Commonwealth Seniors Health Card. They will never be income tested and will retain the card indefinitely (provided they continue to meet all other eligibility requirements. The Low Income Health Care Card provides cheaper medicines under the Pharmaceutical Benefits Scheme; as well as other concessions offered by private companies; plus state and territory government and local council concessions, such as energy and electricity bills, health care costs (including ambulance and dental and eye care), public transport costs, educational fees, and water rates. The Commonwealth Seniors Health Card provides similar benefits to the Low Income Health Care Card, in regards to medical and government concessions or discounts. For those clients that will retain their Age Pension entitlements, but at a reduced level, you will need to consider your ongoing living expenses and cashflow position, and consider where you are able to draw additional monies from to keep your ongoing cashflow unchanged (i.e. increased super drawings, cash at bank, selling shares). As the changes will come into force shortly, we recommend that you contact us to discuss how the changes will affect you personally, and any changes that may need to be implemented prior to 1 January 2017. Please note, these changes will also affect those clients on other Centrelink pensions, including Disability Support Pensions and Carer Payments.

Until next time,

Jonathan Dunne CFP DipFP JP

Authorised Representative for

Financial Wisdom Limited

|